DGR Status for Community Foundations: A Critical Reform to Grow Philanthropy

18 October 2016 at 8:20 am

Community foundations play a critical role, but current tax laws are blocking their access to donors, writes Philanthropy Australia’s Krystian Seibert.

Deductible gift recipient (DGR) status is sought after by charities as it helps attract donors if they can get a tax deduction for their donation.

Unfortunately, our DGR framework is very complicated and has developed in an ad hoc manner – something I’ve written about previously. More than half of all charities can’t even get DGR status.

But even if you do get DGR status, that doesn’t always mean it’s smooth sailing from there. That’s because our tax laws require some charities with DGR status to say no to some donations. That’s the case for community foundations.

As independent and community managed philanthropic organisations, they play an important role partnering with other community organisations to help build more resilient and vibrant communities.

Community foundations generally operate a “public ancillary fund”. They’re regarded as so-called “funding DGRs” whose purpose is to accept donations and make grants to so-called “Item 1” or “doing DGRs”.

Currently, our tax laws make life very hard for community foundations.

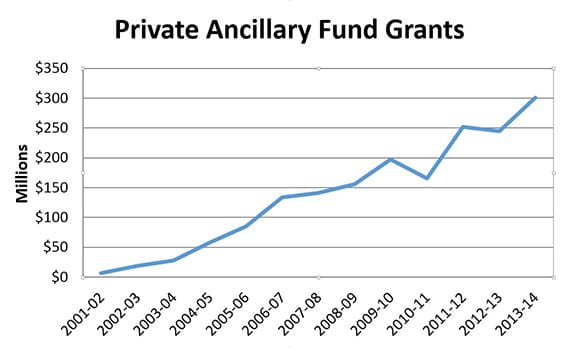

That’s because one of the most common forms of private foundation, private ancillary funds, can’t donate to public ancillary funds. This means that public ancillary funds and the community foundations which operate them are completely cut off from a large chunk of Australian philanthropy. Private ancillary funds gave grants worth $300 million in 2013/14 – and as shown in the chart below, that figure has been steadily growing. Urban community foundations can’t access a single cent of that. The problem is less acute for rural and regional community foundations, as they can access PAF funding via the Foundation for Rural and Regional Renewal’s DGR status and donation account facility. However this arrangement still has certain limitations which means that it’s not a long-term solution.

Some may argue that this restriction is justifiable – private ancillary funds are also “funding DGRs” and hence should be giving grants to “doing DGRs” rather than other “funding DGRs”. After all, if they just give grants to “funding DGRs” then their money isn’t really doing anything! But this is based on a misunderstanding of the role of community foundations.

Community foundations play a critical role as philanthropic intermediaries – they are certainly more than just “funding DGRs”, they are really “doing DGRs” which add value to every dollar they receive and then grant.

They operate at the grassroots to understand community needs at the coal face, and apply their expertise and experience to make better grants. Many community foundations act as a convenor for collective impact efforts to address complex social challenges – examples of this are the Tomorrow Today Foundation’s Education Benalla Program and the Sydney Community Foundation’s ProjectWOW!.

That’s why many private ancillary funds want to donate to them – so that they can take advantage of their expertise, experience, and local connections to more effectively grant into particular communities.

But our tax laws say they can’t. The image below shows how things just aren’t working properly – it’s a cheque sent to a community foundation which had to be sent back because it came from a private ancillary fund.

It was sent to the Jewish Communal Appeal (JCA), a community foundation serving Sydney’s Jewish community. Private ancillary funds want to contribute to the JCA because they know that it has the expertise and experience to ensure that their donations have the highest impact possible. JCA engages with various Jewish community organisations and monitors changing needs within the Jewish community from year to year and makes grants accordingly.

Some may argue that the private ancillary fund wanting to give to the JCA could just give directly to Jewish community organisations – but that workaround means it won’t benefit from the JCA’s expertise and experience. Or some may say that this particular family should just give a donation to the JCA from outside its private ancillary fund – but the reason people set up private ancillary funds is so they can do their giving through them, and the tax laws should facilitate that giving, rather than stifle it. Unfortunately, the workarounds just aren’t up to it.

So what’s the solution? The fact that under our tax laws certain DGRs can’t accept all legitimate donations means that those tax laws need to change. If we want more and better philanthropy in Australia, we can’t have this kind of red tape clogging up the system.

The solution is to create a new DGR category within the Income Tax Assessment Act 1997 (Cth) specifically for community foundations – which involves a relatively simple amendment to the legislation.

This would mean that community foundations would be classified as so-called “Item 1” or “doing DGRs” and would be able to accept donations from private ancillary funds.

It would also mean that community foundations would be able to make grants to a wider range of organisations. Like private ancillary funds, public ancillary funds can only make grants to “Item 1” or “doing DGRs”, and this can make things difficult for community foundations in rural and regional areas, where there may not be many “Item 1” or “doing DGRs” around. I’ve written about that previously.

An alternative, which isn’t perfect but would still be better than the current situation, would be to allow “Item 2” or “funding DGRs” to grant to other “Item 2” DGRs in certain circumstances. That would at least go part way to addressing the current predicament but it wouldn’t address the issue described in the paragraph above.

Dylan Smith, executive officer of the Fremantle Foundation and chair of Australian Community Philanthropy has commented: “Community foundations work at the grassroots to channel giving to where it’s needed most in local communities – it’s frustrating when we have to say no to donations from private ancillary funds. It means local communities miss out on the benefits of better giving. That’s why a having DGR category for community foundations is so important.”

He’s absolutely right.

If we want tax laws which support rather than inhibit more and better philanthropy, we need change. Creating a new DGR category for community foundations is a straightforward and sensible reform which will help grow philanthropy right across Australia. That’s why it needs to be a priority.

About the author: Krystian Seibert is the policy and research manager at Philanthropy Australia and tweets at @KSeibertAu.